This article will be the first in a 3-part series about buying cars with bad credit. Here, we tackle the what you need to do before you buy a car—primarily, that you successfully apply to and are approved for an auto loan at a decent interest rate. Before reading on, however, keep in mind that if you can avoid buying a car with bad credit, please do.

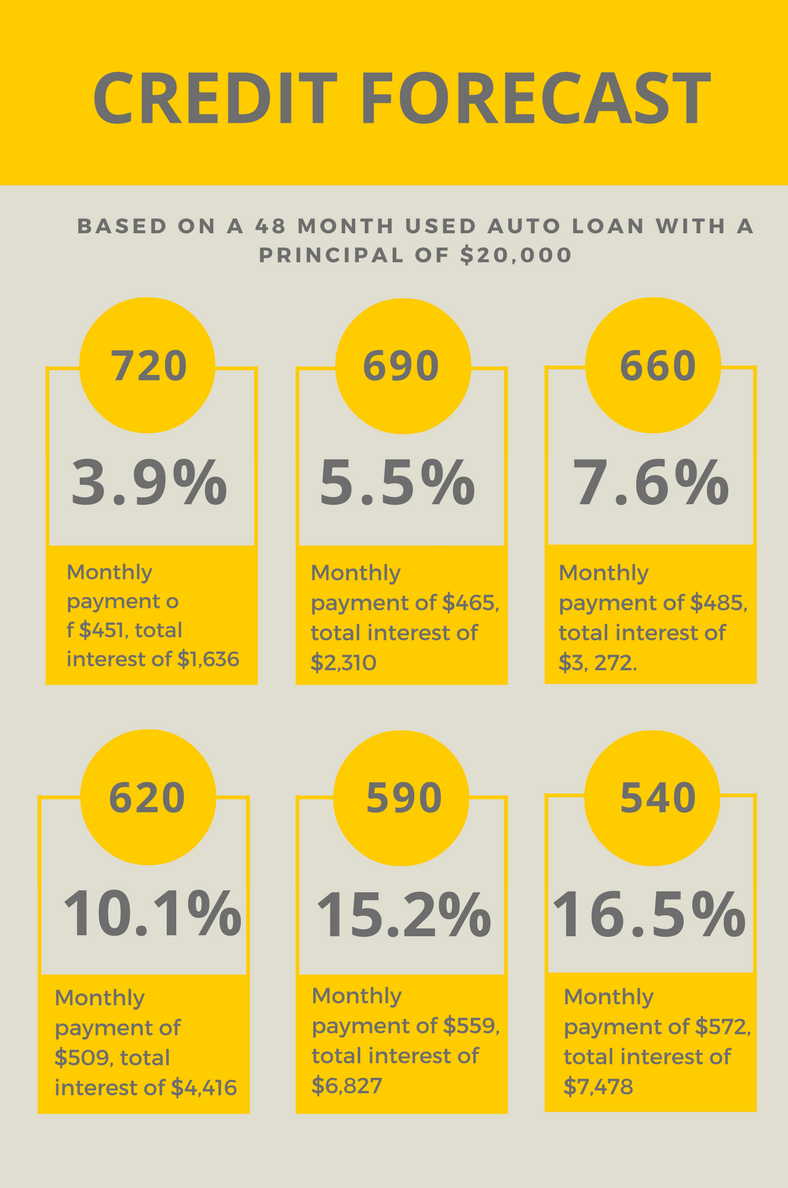

With a score in the low 500s or 600s, you will be looking at starting interest rates of 14% or higher, maybe even an interest rate of 28%. If you can put off buying a car for six months or more, use that time to build up your credit score by using a secured credit card and paying your bills on-time. However, if you must buy a car within the next two months.

Some tips on how to find the best and most affordable auto loan

1. Know Your Credit

You are entitled by law to a free credit report from each of the credit bureaus every 12 months. We recommend checking your credit reports twice a year to avoid falling victim to misreporting by the bureaus or identity fraud. However, when shopping for an auto loan, you should also know your credit score to avoid any misleading deals. The most commonly used scoring model is FICO, however, our website will allow you to pull your credit for free for 7 days. Anything under 629 is usually considered low, and any score lower than 540 is at risk of being denied an auto loan of any kind. However, each lender has a different outlook on your eligibility, so don’t give up right away if your score is in the low 500s and you need a car right away.

2. Shop Around for 2 Weeks

Don’t take the first offer you get (especially if it’s from a dealership), as there might be a better one out there. Apply for auto loans with your local credit union and any credible banks to discuss your options, but be aware that every lender you visit will perform a hard credit inquiry prior to your appointment and that each inquiry has the potential to negatively affect your credit score.

Luckily, most scoring models count every inquiry performed by an auto loan lender in a two-week period as one inquiry only. However, if you extend your search beyond that two-week period because you forgot or were too busy to complete all your appointments within that time frame, your score will suffer. Check your calendar ahead of time to make room in your schedule for multiple appointments with lenders, and leave reminders for yourself about each!

3. Go to Credible Lenders

When obtaining an auto loan, you should always go to credible lenders. You can apply for an auto loan with a bank, credit union, car dealership, or finance company. Apply with institutions that are well-trusted or well-known. Avoid any dealerships, banks, or finance companies which specialize in subprime loans, or loans for people buying with low credit—they might take advantage of you by charging exorbitant or fluctuating interest rates which start at 14% and jump to 17% after your first few payments. We recommend going to a credible credit union, as they are the most likely to offer you a reasonable interest rate based on your credit score and finances.

4. Consider Your Options Carefully

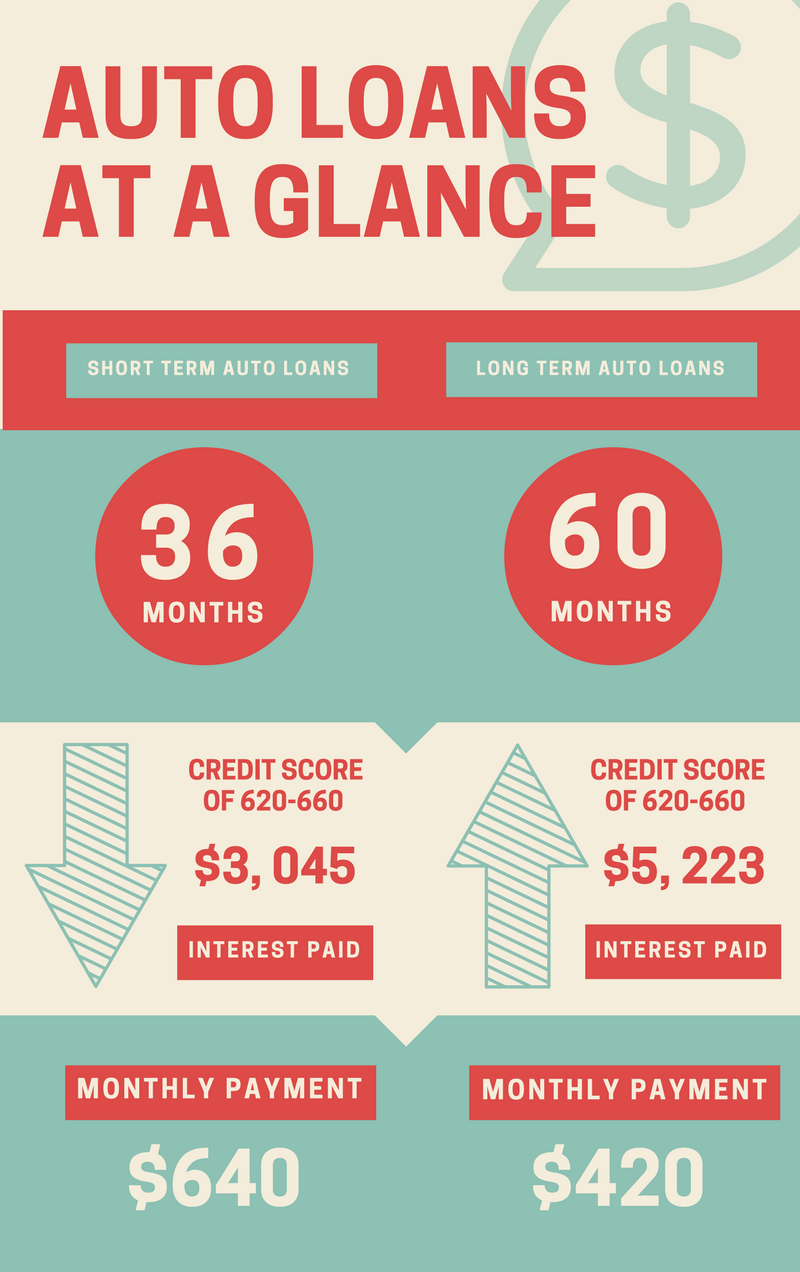

Offers will range from lender to lender and can sometimes be confusing to sort out. One way to categorize multiple offers is to distinguish between long and short-term loans. A short-term loan usually falls within a 3-year period, charges higher monthly payments and down-payments, and offers a lower interest rate. Long-term loans usually fall within a 5-year period, offer lower monthly payments and down payments, and charge higher interest rates.

A higher interest rate will mean paying more for the car once all the expenses are calculated, but keep in mind that you should always take the option which you can afford to make regular, on-time payments for. If a short-term loan with a better interest rate requires monthly payments you know you won’t be able to cover, don’t take it. Missing more payments will only lead to more debt and a lower credit score. However, if you can afford to take the short-term loan with a lower interest rate, go for it; not only will your final bill be smaller, you’ll pay off your car faster and have more time to pay off the other loans and debts hurting your credit score.

5. Prepare Before You Purchase

People buy cars on bad credit all the time. In fact, that’s how many dealerships and lenders make their money—by specializing in selling overpriced cars and auto loans with ridiculous interest rates to people who don’t know any better and are willing to take the first offer that comes their way, no matter how expensive. A poor credit score is often due not only to bad spending habits and a high debt-to-income ratio, but also to a lack of knowledge about credit in general. Becoming informed about credit will help you protect yourself from shady business practices when purchasing loans and help you start repairing your credit score to avoid similar situations in the future.