In the United States, a credit score is a statistical analysis of a person’s credit history used to determine their creditworthiness. It is represented by a numerical value between 300 and 850, with higher values correlating to better creditworthiness. More importantly, it’s how banks, lenders, credit card companies, future employers, and property owners determine whether or not you are likely to pay your bills on time in the future and, consequently, whether or not you are worth doing business with.

Like a bad reputation, bad credit is unlikely to inspire trust in others, especially in the companies with access to such information. Which could mean not getting the credit card you just applied for, or the mortgage you need to finally buy your dream home, or even the job you need to cover all the unpaid bills which continue to harm your credit score.

On the other hand, good credit (like a good reputation, to extend the analogy) comes with extra benefits: lower insurance rates, better employment options, buyer protection against identity theft and fraud, and cheaper initial deposits when renting an apartment or house. Where bad credit can lower your overall quality of life, good credit can make your life not only better, but easier.

The best way to avoid bad credit is to become an educated consumer and to stay informed about your own credit, your civil rights as a consumer with credit, and the practices of the credit industry at large.

1. Knowing Your Own Credit: Credit Reporting and the FICO Score

A credit report is a three-page report generated by one of the credit bureaus. If you’ve ever looked at one, you should already know that they’re notoriously difficult to understand. Credit reports were originally designed as a quick means for creditors and lenders to communicate information about a consumer’s financial history. Consequently, they’re riddled with abbreviations, symbolic markers, and industry jargon which makes reading them feel more like a code-breaking exercise. And as if it weren’t already hard enough for the typical consumer to decipher their credit report, each credit bureau uses its own shorthand system, so learning to read your report from bureau to bureau requires an extensive amount of insider knowledge.

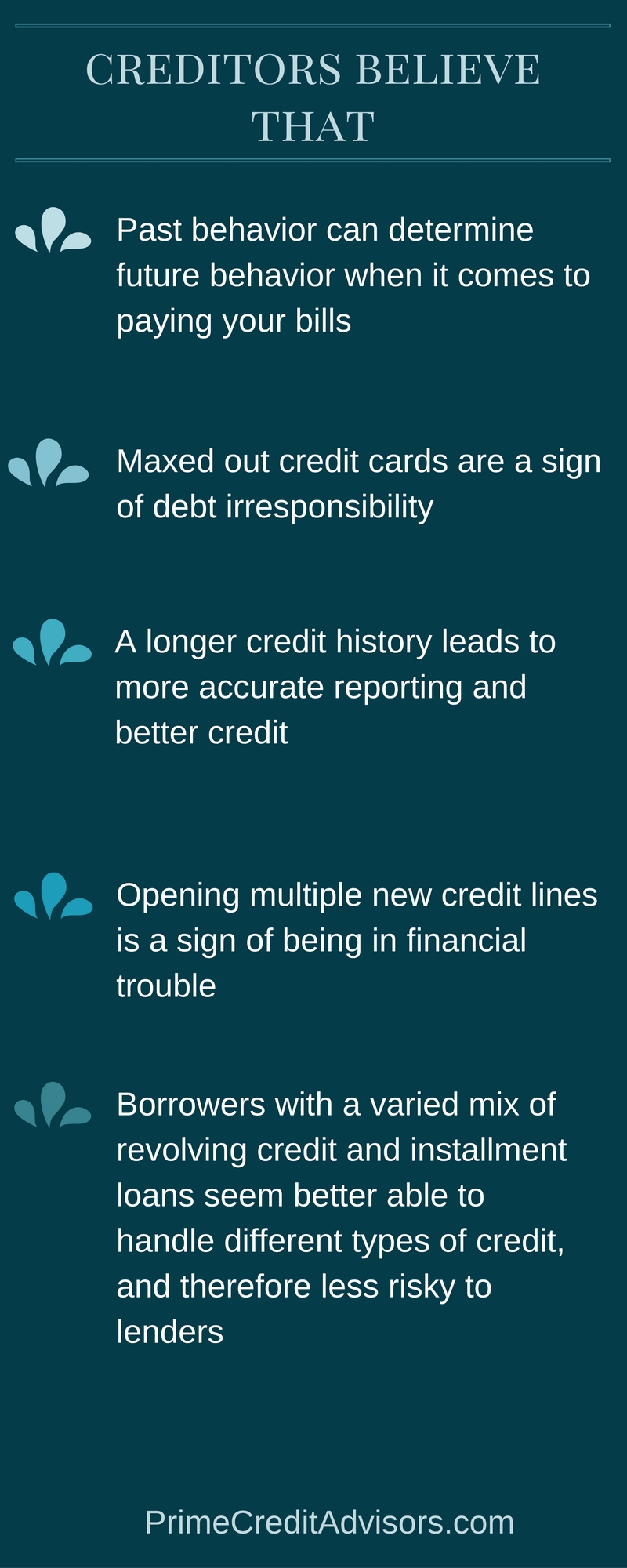

FICO Scores are thankfully much more straightforward. A score between 300 and 850 is assigned to each consumer based on a statistical analysis of their credit report, with 850 being very (pretty much impossibly) good and 300 being the end of your participation in civilized society. Better yet, unlike credit reports, the FICO Score applies the same formula no matter which bureau provides the report. Although the formula itself is a closely-guarded secret, the company behind the FICO score lists the five most important factors determining your score and the reasons behind their inclusion on its website, which we’ve summarized in our infographics (pretty neat, huh?).

FICO Scores are thankfully much more straightforward. A score between 300 and 850 is assigned to each consumer based on a statistical analysis of their credit report, with 850 being very (pretty much impossibly) good and 300 being the end of your participation in civilized society. Better yet, unlike credit reports, the FICO Score applies the same formula no matter which bureau provides the report. Although the formula itself is a closely-guarded secret, the company behind the FICO score lists the five most important factors determining your score and the reasons behind their inclusion on its website, which we’ve summarized in our infographics (pretty neat, huh?).

2. Accessing Your Credit Reports and Score

Under the Fair Credit Reporting Act, U.S. consumers are entitled to a free credit report from each of the three credit bureaus once every twelve months, and can order their free reports through AnnualCreditReport.com. Other circumstances which allow consumers to request and receive a credit report free of charge include if:

- Someone has taken adverse action against you because of information contained in your report

- You are the victim of identity theft and place a fraud alert

- Your report contains inaccurate information due to fraud

- You are on public assistance

- You are unemployed but expect to seek employment within the next 60 days

If none of these situations apply to you, or you’ve requested a report within the last 11 months, you’ll have to pay a fee. Credit reports change continually as you accumulate and pay-off expenses in your day-to-day life, so a report you receive in January could be very different from a report generated in March of the same year. When requesting additional reports, it’s best to go directly through the credit bureaus. Beware of sites offering a free credit report, as the report is often incomplete or temporary and will require a fee for more information.

As for your credit score, you will have to pay for that information no matter who you request it from (bummer). Even sites which claim to offer free credit scores will only provide two credit scores from two of the credit bureaus. However, most companies and employers require scores from all three bureaus, so you’ll have to pay the site for that last score. On average, receiving your full FICO score will cost somewhere between 15$ (if you order directly from the company) and 20$ (if you order from a third-party site like PrivacyGuard.com). Alternatively, you can just wait until your credit statement comes in to check your score, as it will usually be listed at the top of the page.

So now you know how to access your score, as well as what it’s made up of. But what if you get your credit score and it’s far lower than you expected it to be? What do you do then?